热门标签

热门文章

- 1自然语言处理中的深度学习技术和架构

- 2【粉丝福利社】Android应用安全实战:Frida协议分析(文末送书-完结)_frida 拦截所有的安卓网络请求

- 3Spark的基本结构及SparkSQL组件的基本用法_org.apache.spark.sql.types.structtype

- 4Java下的中文分词方案_java bpe中文分词库

- 5FPGA原语IODELAY、ODDR、BUFGMUX和VIVADO BRAM的使用_bufgmux原语

- 6vue中的rules表单校验规则使用方法 rules=“rules“_ rules=";rules_vue2 rules 根据条件验证

- 7Ubuntu下修改docker镜像源_ubuntu docker registry-mirrors需改

- 8项目启动报错:If you want an embedded database (H2, HSQL or Derby), please put it on the classpath

- 9二维码识别与定位-方法2-利用opencv扩展库aruco_aruco二维码定位原理

- 10【数据库设计和SQL基础语法】--表的创建与操作--插入、更新和删除数据_如何在数据表中插入新的数据?插入数据时需要考虑哪些事项

当前位置: article > 正文

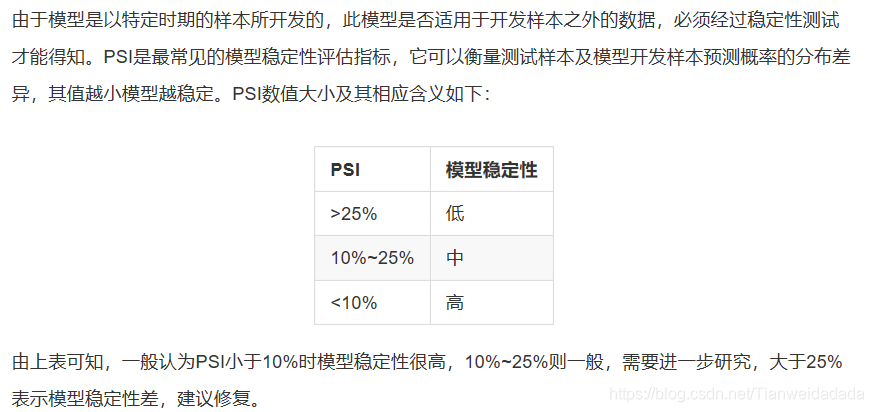

四、大数据实践——模型预测及分析

作者:盐析白兔 | 2024-05-25 09:38:38

赞

踩

四、大数据实践——模型预测及分析

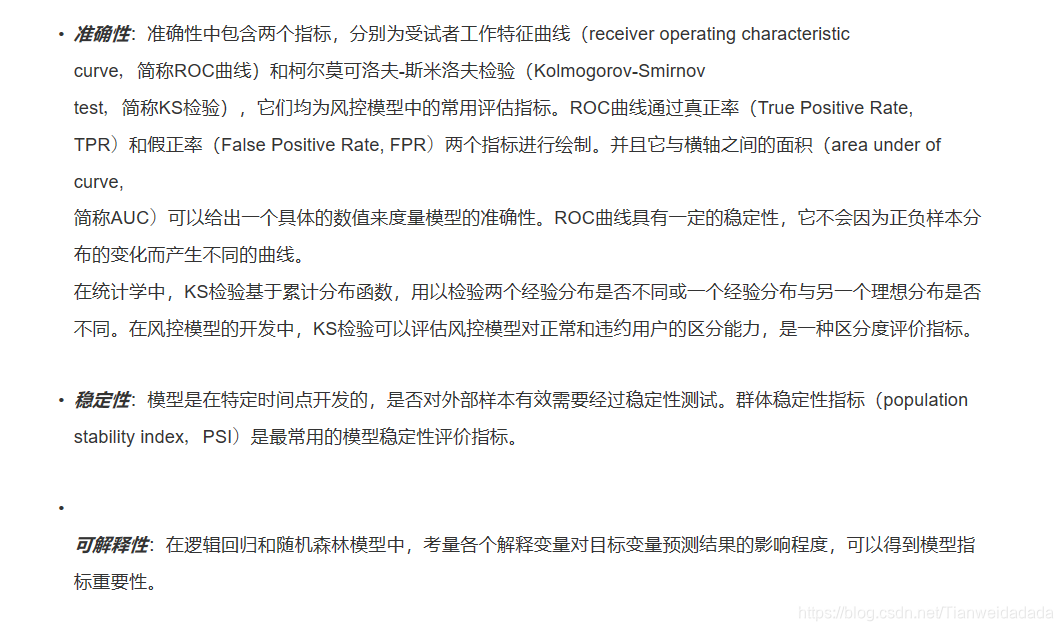

一、风险评估模型的效果评价方法

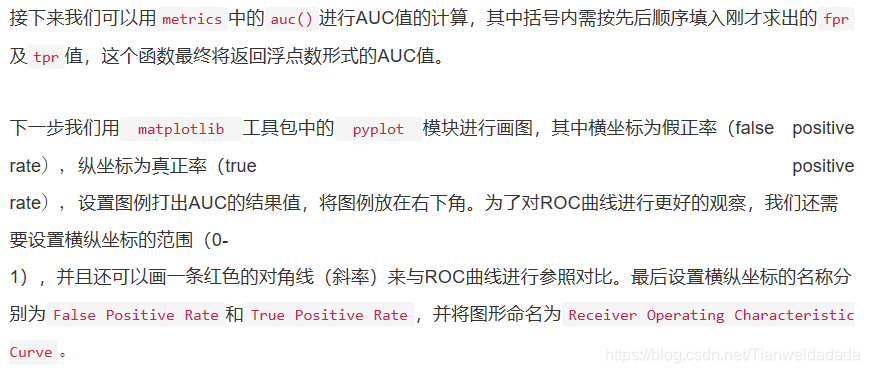

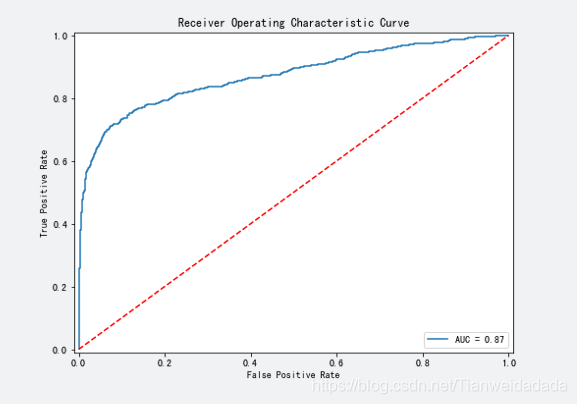

二、利用AUC评估逻辑回归模型的准确性

- #用metrics.roc_curve()求出 fpr, tpr, threshold

- fpr, tpr, threshold = metrics.roc_curve(y_test,y_predict_best)

-

- #用metrics.auc求出roc_auc的值

- roc_auc = metrics.auc(fpr,tpr)

-

- #将图片大小设为8:6

- fig,ax = plt.subplots(figsize=(8,6))

-

- #将plt.plot里的内容填写完整

- plt.plot(fpr, tpr, label = 'AUC = %0.2f' % roc_auc)

-

- #将图例显示在右下方

- plt.legend(loc = 'lower right')

-

- #画出一条红色对角虚线

- plt.plot([0, 1], [0, 1],'r--')

-

- #设置横纵坐标轴范围

- plt.xlim([-0.01, 1.01])

- plt.ylim([-0.01, 1.01])

-

- #设置横纵名称以及图形名称

- plt.ylabel('True Positive Rate')

- plt.xlabel('False Positive Rate')

- plt.title('Receiver Operating Characteristic Curve')

- plt.show()

-

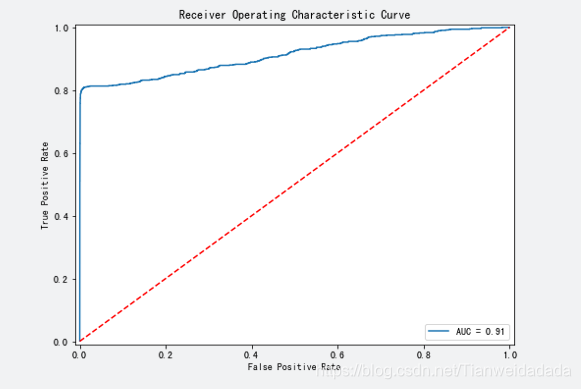

三、利用AUC评估随机森林模型的准确性

- #用metrics.roc_curve()求出 fpr, tpr, threshold

- fpr, tpr, threshold = metrics.roc_curve(y_test,y_predict_best)

-

- #用metrics.auc求出roc_auc的值

- roc_auc = metrics.auc(fpr,tpr)

-

- #将图片大小设为8:6

- fig,ax = plt.subplots(figsize=(8,6))

-

- #将plt.plot里的内容填写完整

- plt.plot(fpr, tpr, label = 'AUC = %0.2f' % roc_auc)

-

- #将图例显示在右下方

- plt.legend(loc = 'lower right')

-

- #画出一条红色对角虚线

- plt.plot([0, 1], [0, 1],'r--')

-

- #设置横纵坐标轴范围

- plt.xlim([-0.01, 1.01])

- plt.ylim([-0.01, 1.01])

-

- #设置横纵名称以及图形名称

- plt.ylabel('True Positive Rate')

- plt.xlabel('False Positive Rate')

- plt.title('Receiver Operating Characteristic Curve')

- plt.show()

-

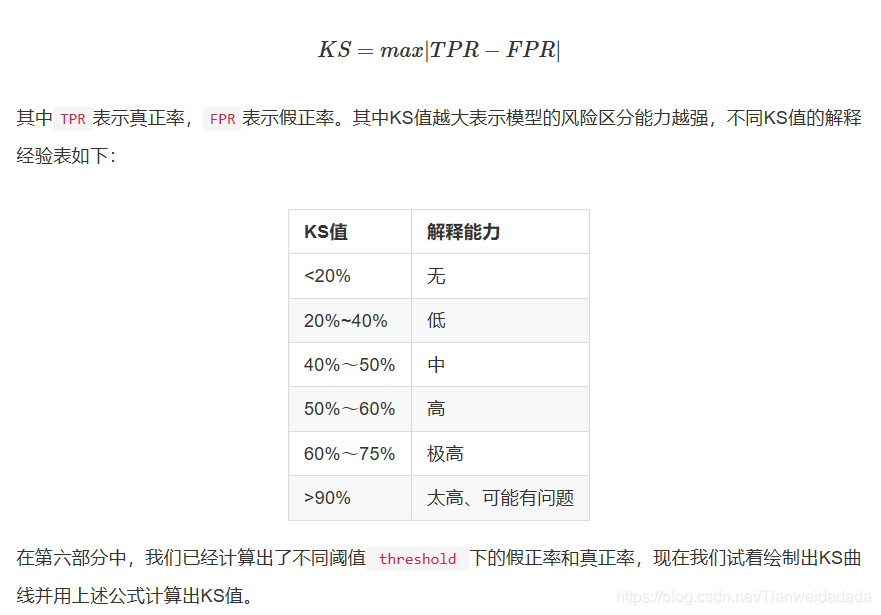

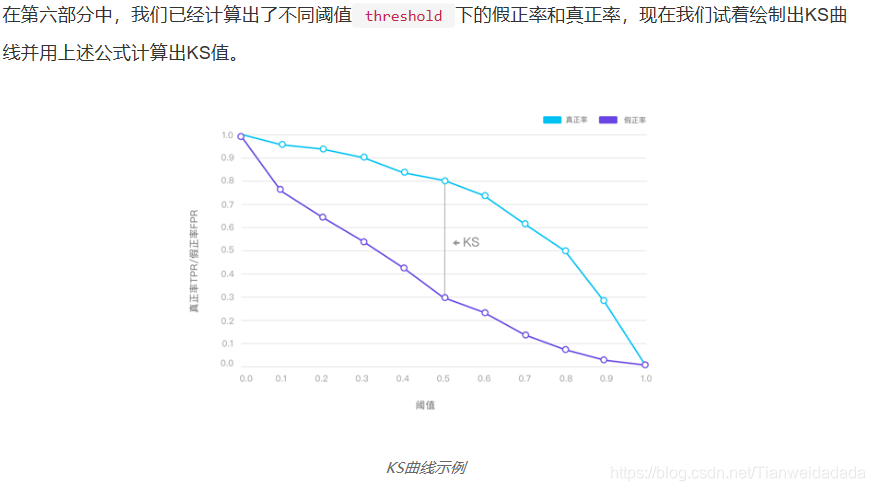

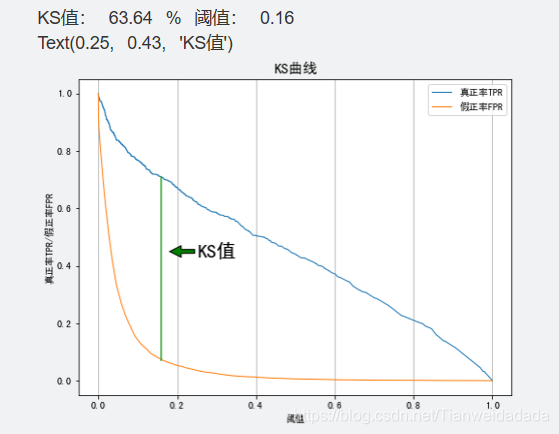

四、利用KS值评估逻辑回归模型的准确性

- #用metric.roc_curve()求出 fpr, tpr, threshold

- fpr, tpr, threshold = metrics.roc_curve(y_test, y_predict_best)

- #print(threshold)

- #求出KS值和相应的阈值

- ks = max(abs(tpr-fpr))

- thre = threshold[abs(tpr-fpr).argmax()]

-

- ks = round(ks*100, 2)

- thre = round(thre, 2)

- print('KS值:', ks, '%', '阈值:', thre)

-

- #将图片大小设为8:6

- fig = plt.figure(figsize=(8,6))

- #将plt.plot里的内容填写完整

-

- plt.plot(threshold[::-1], tpr[::-1], lw=1, alpha=1,label='真正率TPR')

- plt.plot(threshold[::-1], fpr[::-1], lw=1, alpha=1,label='假正率FPR')

-

-

- #画出KS值的直线

- ks_tpr = tpr[abs(tpr-fpr).argmax()]

- ks_fpr = fpr[abs(tpr-fpr).argmax()]

- x1 = [thre, thre]

- x2 = [ks_fpr, ks_tpr]

- plt.plot(x1, x2)

-

- #设置横纵名称以及图例

- plt.xlabel('阈值')

- plt.ylabel('真正率TPR/假正率FPR')

- plt.title('KS曲线', fontsize=15)

- plt.legend(loc="upper right")

- plt.grid(axis='x')

-

- # 在图上标注ks值

- plt.annotate('KS值', xy=(0.18, 0.45), xytext=(0.25, 0.43),

- fontsize=20,arrowprops=dict(facecolor='green', shrink=0.01))

五、利用KS值评估随机森林模型准确性(code同上)

六、利用PSI评估逻辑回归模型稳定性

- ## 训练集预测概率

- y_train_probs = lr.predict_proba(x_train)[:,1]

- ## 测试集预测概率

- y_test_probs = lr.predict_proba(x_test)[:,1]

-

- def psi(y_train_probs, y_test_probs):

- ## 设定每组的分点

- bins = np.arange(0, 1.1, 0.1)

-

- ## 将训练集预测概率分组

- y_train_probs_cut = pd.cut(y_train_probs, bins=bins, labels=False)

- ## 计算预期占比

- expect_prop = (pd.Series(y_train_probs_cut).value_counts()/len(y_train_probs)).sort_index()

-

- ## 将测试集预测概率分组

- y_test_probs_cut = pd.cut(y_test_probs, bins=bins, labels=False)

- ## 计算实际占比

- actual_prop = (pd.Series(y_test_probs_cut).value_counts()/len(y_test_probs)).sort_index()

-

- ## 计算PSI

- psi = ((actual_prop-expect_prop)*np.log(actual_prop/expect_prop)).sum

-

- return psi, expect_prop, actual_prop

-

- ## 运行函数得到psi、预期占比和实际占比

- psi, expect_prop, actual_prop = psi(y_train_probs,y_test_probs)

- print('psi=',psi)

-

- ## 创建(12, 8)的绘图框

- fig = plt.figure(figsize=(12, 8))

-

- ## 设置中文字体

- plt.rcParams['font.sans-serif'] = ['SimHei']

- plt.rcParams['axes.unicode_minus'] = False

-

- ## 绘制条形图

- plt.bar(expect_prop.index + 0.2, expect_prop, width=0.4, label='预期占比')

- plt.bar(actual_prop.index - 0.2, actual_prop, width=0.4, label='实际占比')

- plt.legend()

-

- ## 设置轴标签

- plt.xlabel('概率分组', fontsize=12)

- plt.ylabel('样本占比', fontsize=12)

-

- ## 设置轴刻度

- plt.xticks([0, 1, 2, 3, 4, 5, 6, 7, 8, 9],

- ['0-0.1', '0.1-0.2', '0.2-0.3', '0.3-0.4', '0.4-0.5', '0.5-0.6', '0.6-0.7', '0.7-0.8', '0.8-0.9', '0.9-1'])

-

- ## 设置图标题

- plt.title('预期占比与实际占比对比条形图', fontsize=15)

-

- ## 在图上添加文字

- for index, item1, item2 in zip(range(10), expect_prop.values, actual_prop.values):

- plt.text(index+0.2, item1 + 0.01, '%.3f' % item1, ha="center", va= "bottom",fontsize=10)

- plt.text(index-0.2, item2 + 0.01, '%.3f' % item2, ha="center", va= "bottom",fontsize=10)

-

-

七、计算逻辑回归指标重要性

- from sklearn.linear_model import LogisticRegression

- lr_clf = LogisticRegression(penalty='l1',C = 0.6, random_state=55)

- lr_clf.fit(x_train, y_train)

-

- # 查看逻辑回归各项指标系数

- coefficient = lr_clf.coef_

-

- # 取出指标系数,并对其求绝对值

- importance = abs(coefficient)

-

- # 通过图形的方式直观展现前八名的重要指标

- index=data.drop('Default', axis=1).columns

- feature_importance = pd.DataFrame(importance.T, index=index).sort_values(by=0, ascending=True)

-

- # # 查看指标重要度

- print(feature_importance)

-

- # 水平条形图绘制

- feature_importance.tail(8).plot(kind='barh', title='Feature Importances', figsize=(8, 6), legend=False)

- plt.show()

八、计算随机森林的指标重要性

- from sklearn.ensemble import RandomForestClassifier

- rf = RandomForestClassifier(n_estimators = 150, criterion = 'entropy', max_depth = 5, min_samples_split = 2, random_state=12)

- rf.fit(x_train, y_train)

-

- # 查看随机森林各项指标系数

- importance = rf.feature_importances_

-

- # 通过图形的方式直观展现前八名的重要指标

- index=data.drop('Default', axis=1).columns

- feature_importance = pd.DataFrame(importance.T, index=index).sort_values(by=0, ascending=True)

-

- # # 查看指标重要度

- print(feature_importance)

-

- # 水平条形图绘制

- feature_importance.tail(8).plot(kind='barh', title='Feature Importances', figsize=(8, 6), legend=False)

- plt.show()

声明:本文内容由网友自发贡献,不代表【wpsshop博客】立场,版权归原作者所有,本站不承担相应法律责任。如您发现有侵权的内容,请联系我们。转载请注明出处:https://www.wpsshop.cn/w/盐析白兔/article/detail/621536

推荐阅读

相关标签